By Melanie Buffel, B.A. Psych, MBA candidate

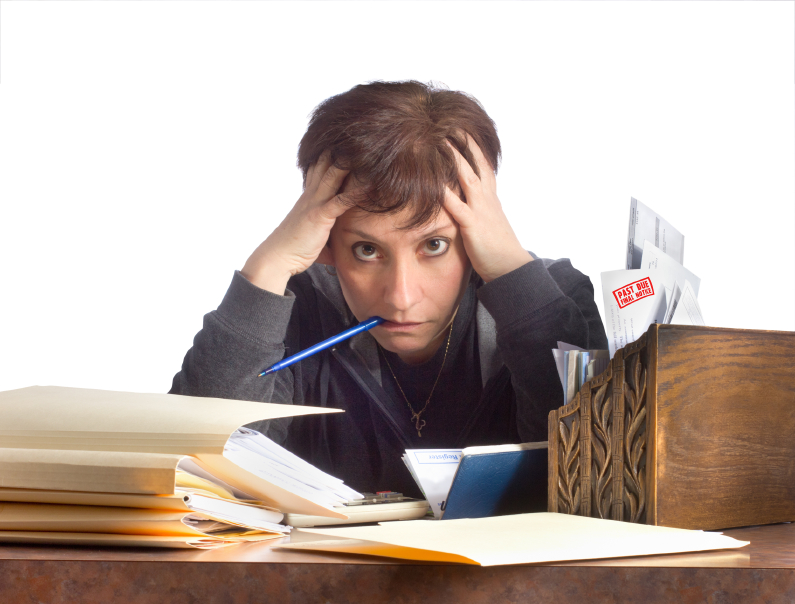

Our culture is rife with mixed messages about money. Money is freedom, money is greed, live simply – but to be happy you’ll need this car, have these clothes and that phone. Yet one message comes through loud and clear; don’t talk about money – at least not at the personal level.

On a broader scale we talk about money all the time. The financial media talks about the level of consumer debt that Canadians carry, or how unprepared many people are for retirement, while at the same time new homes seem to get bigger, and Facebook is full of vacation and home renovation photos. We hear that people are struggling but we don’t see it. We commiserate with friends that gas and groceries are too expensive, or that university tuition for our kids is weighing us down, but we often do that over a nice glass of wine or an overpriced coffee. Everyone we know seems fine. The thing is, behind closed doors, not everybody feels fine. Many people feel overwhelmed and stressed, but are too embarrassed or ashamed to tell anyone. The isolation goes even deeper if financial worries are being kept from people otherwise close to you, such as a spouse, close friends or family.